For much of the past two years, M&A markets were not constrained by a lack of capital or strategic intent, but by economics that simply did not work. Rising interest rates increased the cost of leverage, compressed debt capacity, and widened valuation gaps between buyers and sellers. Transactions still occurred, but selectively, favoring only the highest-quality assets or buyers with differentiated access to capital.

That backdrop began to shift in late 2025. In December, the Federal Reserve lowered the federal funds target range to 3.50%–3.75%, following a prolonged tightening cycle, and then held rates steady in January 2026 while emphasizing data dependence going forward (Federal Reserve, FOMC statements). At the same time, the effective federal funds rate declined from roughly 4.2% in September 2025 to the mid-3.6% range by early 2026, materially easing short-term funding costs (Federal Reserve Bank of St. Louis, FRED).

Immediately prior to these moves, M&A activity was defined by friction. Higher benchmark rates pushed borrowing costs up across the capital stack, forcing buyers to prioritize debt service coverage over growth and limiting achievable leverage. According to Federal Reserve data, short-term policy rates sat at multi-decade highs through much of 2024–2025, pressuring leveraged underwriting and driving more conservative credit structures. Financing remained available, but underwriting tightened, timelines lengthened, and earnouts, seller notes, and contingent consideration became standard tools to bridge valuation gaps.

The Fed’s late-2025 easing has meaningfully improved that math. Lower base rates reduce interest expense, improve coverage ratios, and expand feasible leverage – even without aggressive assumptions. Just as important, the Fed’s subsequent pause provides stability. In M&A, predictability around financing costs often matters as much as the level itself. Deals that struggled to clear investment committee thresholds only months earlier now pencil with more conventional structures.

For 2026, expectations point to a constructive but disciplined recovery. Major advisory firms project modest growth in deal volume alongside continued strength in deal value, reflecting concentration in larger, strategic transactions rather than a broad-based surge. The middle market stands to benefit disproportionately as financing conditions normalize and sidelined processes return. Private equity sponsors, holding historically high levels of undeployed capital, are expected to re-engage on exits and recapitalizations as leverage economics improve. Corporates, meanwhile, are revisiting carve-outs and targeted acquisitions as lower rates make separation costs and bolt-on strategies more financeable.

This is not a return to the zero-rate era. Regulatory scrutiny remains elevated, lenders remain selective, and execution risk continues to command a premium. But the removal of a critical constraint – punitive financing costs – changes behavior at the margin. In a market where marginal improvements unlock activity, that change is significant.

The Fed’s recent rate cuts do not guarantee a surge in M&A, but they decisively improve transactability. With borrowing costs lower and policy more predictable, 2026 is shaping up as a year in which more deals clear, more buyers participate, and valuation expectations realign. For prepared sellers and disciplined acquirers, the window is reopening – and this time, the math works.

M&A Market Activity

U.S. deal volume declined by 2.7 percent in January 2026 compared to the same period last year. Despite this, the underlying conditions for M&A are improving rather than deteriorating. Early-year activity continues to reflect the lagged effects of a higher-rate environment, conservative credit underwriting, and transactions deferred through much of 2025. However, with borrowing costs now meaningfully lower and rate volatility reduced following the Federal Reserve’s recent easing, confidence is gradually returning to boardrooms and investment committees. As financing economics normalize, a growing pipeline of postponed middle-market transactions, sponsor exits, and corporate carve-outs is expected to come back to market later in 2026, positioning deal volume for a more sustained recovery beyond the first quarter.

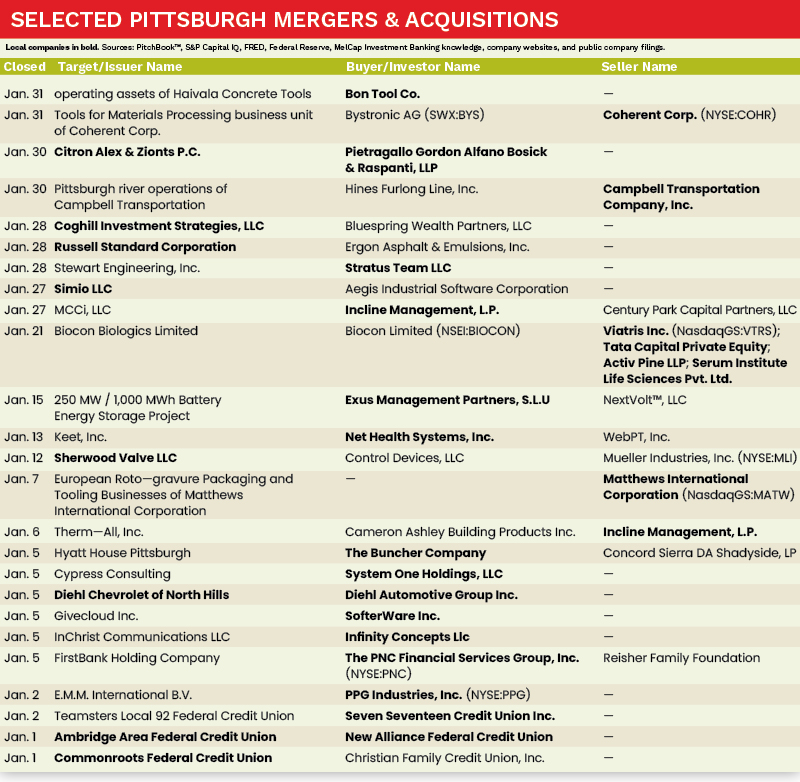

The Pittsburgh M&A market experienced a 56.3 percent increase in activity in January 2026 compared to the same period in 2025 with several noteworthy transactions completed by both strategic acquirers and private equity firms. Incline Equity Partners, PPG Industries, Net Health Systems, and System One Holdings all completed strategic acquisitions.

Deal of the Month

On January 27, 2026, Pittsburgh-based Incline Equity Partners, a leading private equity firm dedicated to investing across the middle market, announced its investment in MCCi, a provider of enterprise content management and workflow automation solutions to public sector clients.

Headquartered in Tallahassee, FL, MCCi’s comprehensive suite of products enables state and local governments to solve manual workflow challenges and drive operational efficiency throughout their organizations. The Company’s best-in-class solutions and high touch customer service help clients address regulatory-driven needs within their document management, records request management and licensing and permitting processes.

“MCCi has earned a strong reputation for delivering high-quality service and support that has led to long-term client relationships,” said David Chen, Managing Director at Incline. “We plan to pursue opportunities to enhance the Company’s core automation platform and add complementary software solutions.”

Sources: PitchBook™, S&P Capital IQ, FRED, Federal Reserve, MelCap Investment Banking knowledge, company websites, and public company filings.

Andrew J. Chalhoub is a Senior Associate at MelCap Partners, LLC, a middle-market investment banking advisory firm. For more information on MelCap Partners, please visit www.melcap.com or email [email protected].