In middle-market M&A transactions, buyers are increasingly prioritizing partnerships with owners who are willing to remain involved in the business after closing. Rather than pursuing a complete exit, many founders and shareholders are choosing to stay engaged operationally while retaining an ownership stake through rollover equity. This structure has become particularly common in private equity transactions, where long-term value creation often depends on continuity within management and alignment between both parties.

A rollover occurs when a seller reinvests a portion of their sale proceeds back into the company as equity in the new ownership structure. Instead of receiving 100 percent cash at close, the owner retains a minority interest and participates in the company’s future growth alongside the buyer. In many transactions, this retained stake represents a meaningful portion of the total equity value.

For buyers, an owner’s continued involvement can significantly reduce transition risk. Existing management teams often hold decades of customer relationships, industry expertise and operational knowledge that are difficult to replace immediately following an acquisition. Keeping ownership involved helps maintain stability within the organization and allows the business to continue operating with minimal disruption.

Private equity firms often view the exiting shareholders and management teams as critical partners in executing the next stage of growth. With additional capital and strategic resources available post-close, buyers frequently look to existing leadership teams to help expand operations, pursue acquisitions or improve operational efficiency. A rollover structure reinforces this partnership by ensuring both parties remain focused on increasing long-term enterprise value.

From the seller’s perspective, remaining involved can offer both financial and strategic benefits. Owners who believe in the future trajectory of the business may view rollover equity as an opportunity to participate in additional upside as the company grows. In successful investments, the retained equity stake can generate meaningful proceeds in a future liquidity event, often several years after the initial transaction.

Additionally, rollover structures have become increasingly useful in today’s financing environment. As lending markets have tightened and transaction structures have become more creative, buyers have utilized rollover equity to reduce upfront cash requirements while still delivering competitive overall valuations.

As a result, rollover equity and ongoing owner participation have evolved from niche transaction features into standard components of many middle-market deals. When aligned properly, these structures can create a smoother ownership transition, stronger long-term incentives and a shared commitment to future growth.

M&A Market Activity

U.S. M&A transaction volume remained relatively stable through April 2026 compared to the same period last year, declining only modestly by 3.4 percent, reflecting continued market resiliency and steady demand from both strategic and financial buyers. While financing conditions have gradually improved, buyers across the middle market continued to maintain disciplined underwriting standards, with ongoing emphasis placed on earnings quality, cash flow stability and downside protection amid broader economic uncertainty.

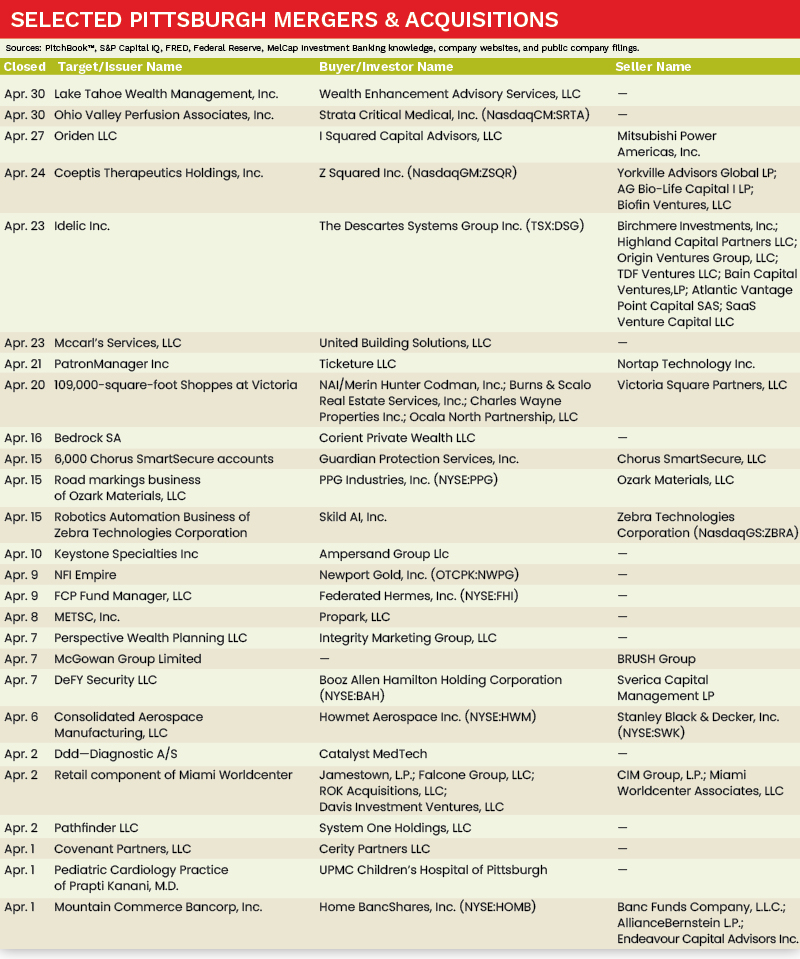

The Pittsburgh M&A market experienced strong activity in April 2026, with several noteworthy transactions completed by both strategic acquirers and private equity firms. Local companies, including Federated Hermes, Inc., PPG Industries, Inc., and Guardian Protection Services, Inc., all completed strategic acquisitions.

Deal of the Month

In April, Howmet Aerospace Inc., a leading provider of advanced engineered solutions for the aerospace and transportation industries, finalized the acquisition of Consolidated Aerospace Manufacturing from Stanley Black & Decker, Inc.

CAM is a global designer and manufacturer of precision fasteners, fluid fittings, and other highly engineered components used in demanding aerospace and defense applications. The acquisition strengthens Howmet’s portfolio of mission-critical aerospace fastening solutions and expands its exposure to key commercial aerospace and defense platforms.

John C. Plant, Executive Chairman and CEO of Howmet Aerospace, stated, “CAM’s established brands, engineering prowess, and deep customer relationships are a perfect complement to our existing business. This transaction will allow us to better serve our aerospace and defense customers with a broader offering of mission-critical fastening solutions and represents a compelling use of capital to drive value for our shareholders.”

Sources: PitchBook™, S&P Capital IQ, FRED, Federal Reserve, MelCap Investment Banking knowledge, company websites, and public company filings.

Carter Hatina is a Vice President at MelCap Partners, LLC, a middle-market investment banking advisory firm. For more information on MelCap Partners, please visit www.melcap.com or email [email protected].