he lower middle market continues to experience a persistent disconnect between seller valuation expectations and buyer discipline, even as financing conditions have improved and capital markets have become more accommodating. Following a period defined by elevated interest rates, tighter credit availability and increased economic uncertainty, transaction activity slowed and pricing expectations became increasingly misaligned. Although access to capital has improved and lenders have returned to the market with greater confidence, the valuation gap has not materially narrowed. Instead, it is manifesting itself through more selective negotiations, heightened diligence and increasingly creative deal structures rather than broad-based multiple expansion.

The practical reality is that capital has returned, but it is being deployed with a high degree of selectivity. Many buyers spent the previous cycle focused on portfolio integration, balance sheet preservation, operational efficiency and more rigorous underwriting standards. That discipline has not faded with the return of liquidity. If anything, it has become further ingrained in acquisition strategies. As a result, capital is increasingly concentrated in businesses that demonstrate consistent earnings performance, durable cash flow generation and clear competitive positioning within their respective markets.

This dynamic is particularly evident in the way acquisition opportunities are being evaluated. Buyers are placing greater emphasis on recurring revenue streams, margin stability, customer retention and predictable operating performance. At the same time, they are carefully assessing customer concentration risks, exposure to fluctuating input costs, management depth and the credibility of forward-looking growth projections. High-quality businesses continue to attract significant interest and competitive bidding environments, while average businesses often face longer sale processes, more extensive diligence requirements, and increased negotiation around both valuation and transaction structure. As a result, valuation is becoming more directly tied to earnings quality and business durability rather than headline market multiples. Even with improved financing availability, buyers remain reluctant to stretch on price without meaningful structural protections. Earnouts, seller financing, rollover equity and contingent consideration mechanisms have become increasingly common tools for bridging valuation gaps while preserving transaction feasibility and aligning incentives between buyers and sellers.

The availability of capital fosters healthy M&A activity levels, however, investment dollars are disproportionately flowing toward higher-quality assets with demonstrated resilience and predictable performance. As such, the outcome is a widening divide between companies that command premium valuations and competitive buyer interest, and those that require greater flexibility on price, terms or structure to complete a transaction.

Ultimately, the core tension remains unchanged. Seller expectations and buyer discipline are still not fully aligned. While improved liquidity continues to support deal activity across the lower middle market, successful outcomes are increasingly determined by business quality, risk profile, earnings visibility and transaction structure rather than a rising valuation environment. In today’s market, preparation, positioning and the ability to clearly demonstrate sustainable value creation have become critical differentiators in achieving premium outcomes.

M&A Market Activity

U.S. deal volume declined 14.9 percent in May 2026 compared to the same period in the prior year, reflecting a more cautious transaction environment amid persistent economic uncertainty, ongoing valuation mismatches between buyers and sellers, and financing costs that remain elevated relative to historical levels. Geopolitical developments and evolving policy considerations also contributed to longer transaction timelines and delayed decision-making, particularly for larger and more complex deals. Despite the decline in completed transactions, underlying market conditions remain constructive. Stabilizing interest rates, ample private credit availability and significant private equity dry powder continue to support acquisition activity, while strategic buyers remain focused on acquiring technology, talent and growth capabilities. As market confidence improves and valuation expectations align, M&A activity is expected to gradually recover through the remainder of fiscal year 2026.

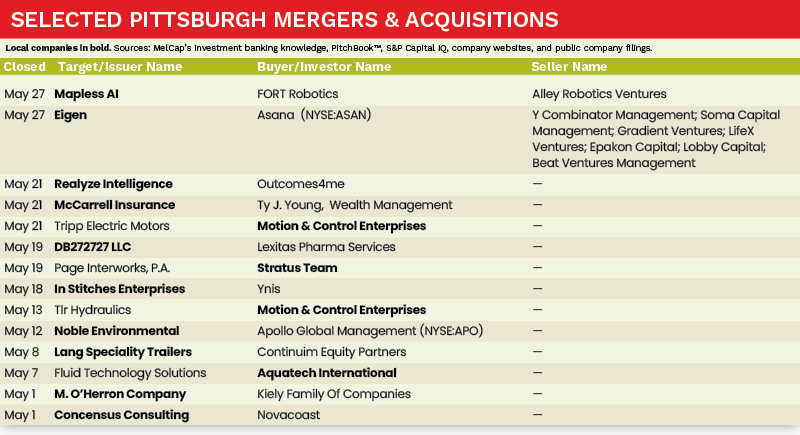

In May 2026, the Pittsburgh M&A market saw continued expansion, with year-over-year deal volume increasing by 7.7 percent compared to the same period in the previous year. Local companies, including Motion & Control Enterprises, Aquatech International, and Stratus Team, all completed strategic acquisitions.

Deal of the Month

On May 7, 2026, Canonsburg, Pennsylvania-based Aquatech International announced its acquisition of FTS H2O, a leader in membrane-based brine concentration and resource recovery technologies. The transaction enhances Aquatech’s capabilities in lithium processing, critical minerals recovery, zero liquid discharge (ZLD), and sustainable water management solutions. By integrating FTS H2O’s advanced membrane technologies with Aquatech’s global engineering and execution platform, the combined company is positioned to deliver more energy-efficient and environmentally sustainable solutions for industrial water treatment and resource recovery applications. The acquisition also strengthens Aquatech’s presence in high-growth markets driven by increasing demand for critical minerals, water reuse, and sustainable industrial processes worldwide.

Sources: MelCap’s investment banking knowledge, PitchBook™, S&P Capital IQ, company websites, and public company filings.

Domenick Cristino is a Director at MelCap Partners, LLC, a middle-market investment banking advisory firm. For more information on MelCap Partners, please visit www.melcap.com or email [email protected].