Despite concerns of the global economy entering into a recessionary cycle, due to mounting headwinds including accelerating inflation, rising interest rates, a lower equity market, and a continued energy crisis, many companies are confronted with an ongoing labor shortage. Stemming from the COVID-19 pandemic, many employees have not reentered the market by choice or through early retirement, now known as the “Great Resignation”, which can be observed by the nearly record number of U.S. job openings. Through April 2022, and updated as of June 2022, the number of U.S job openings was observed at 11.4 million – just short of the record of March 2022 of 11.9 million. According to PWC’s Global M&A Industry Trends: 2022 mid-year update, the number one risk factor to growth for companies is the workforce primarily driven by the “Great Resignation” and the highest wage inflation in decades. As a result, acquisitions have become a focus for workforce strategy.

Holistically, strategic and financial buyers have had to realign acquisition strategies to place a greater emphasis on targeting quality companies with strong, stable workforces as a means to identify top talent and enhance overall human capital. From a sellers’ perspective, companies that employ quality workforces and have demonstrated a history of positive financial performance are in a marketable position to take advantage of the continued lofty valuations. These valuations are primarily due to the excess liquidity that remains in the market. According to PitchBook, global dry powder in Q2 2022 exceeded $2 trillion, 3x higher than during financial crisis, and over $600 billion within the U.S. through Q1 2022. Additionally, U.S. cash on corporate or strategic balance sheets exceeded $1.9 trillion in the U.S. alone.

M&A Activity

Following healthy M&A deal flow in the U.S. throughout the first quarter of 2022, deal volume has declined in recent months. U.S. M&A deal volume for the second quarter ended June 30, 2022 was 15.2% lower than the same period in 2021, while deal volume for the six months ended June 2022 was 7.2% lower than the same period in 2021. Disclosed deal value within the U.S. M&A market, however, has increased by 79.4% for the six months ended June 2022 when compared with the same period in 2021.

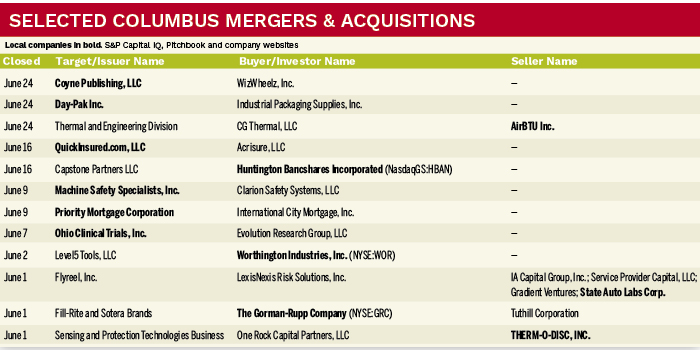

More specifically, Central Ohio continues to navigate similar turbulence experienced by the broader U.S. M&A market, as deal volume for the three months ended June 30, 2022 was 15.2% lower than the same period in 2021. With that being said, Central Ohio experienced a number of transactions in June 2022 from reputable strategic buyers such as, but not limited to, the following businesses: The Gorman-Rupp Company and Worthington Industries.

Evan Lyons is a senior associate and Mike Kostandaras is an analyst with MelCap Partners LLC, a middle-market investment banking advisory firm. For more information on MelCap Partners, visit www.melcap.com or email [email protected]