For decades, private equity operated on a simple premise: acquire, build, and exit within a defined fund lifecycle. Today, that model is being quietly but decisively rewritten. Continuation funds — GP-led vehicles that transfer select portfolio assets into a new fund structure — have evolved from a niche workaround into one of the most consequential innovations in modern private markets.

The numbers tell a compelling story. Total secondary transaction volume reached $162 billion in 2024 — a 45 percent increase from the prior year and more than four times the market’s size a decade ago, when volume stood at just $40 billion. GP-led transactions, of which continuation funds are the dominant structure, accounted for $75 billion of that total, representing nearly half of all secondary activity. Single-asset continuation vehicles alone comprised approximately 48 percent of GP-led volume in 2024.

The drivers are structural. With public equity markets remaining an inconsistent exit path and strategic acquirers increasingly disciplined on valuation, general partners managing genuinely exceptional assets face a difficult choice: divest prematurely at a discount, or seek an alternative. Continuation funds offer another option — transferring assets into a new vehicle, providing liquidity to existing limited partners who wish to exit, while preserving the investment for those with continued conviction. The growing appetite for this solution is reflected in the data: 46 percent of respondents in Dechert’s 2026 Global Private Equity Outlook survey reported utilizing GP-led secondaries or continuation vehicles to manage fundraising challenges, which was nearly double the prior year’s figure.

The trajectory of growth shows little sign of flattening. The first half of 2025 set a new record, with total secondary transaction volume reaching $103 billion — a 51 percent increase over H1 2024 — placing the market on pace to exceed $210 billion for the full year. Dry powder available to secondaries buyers has reached an estimated $315 billion as of Q3 2025, and many within the industry have projected annual deal value could approach $400 billion by 2030.

For investment banks, this evolution has created a distinct and growing advisory mandate. Fairness opinions, LP tender processes, secondary market pricing, and conflict management between legacy and incoming investors have each become specialized disciplines commanding meaningful fees and senior attention.

The central question now is one of governance. Regulators and institutional investors are applying greater scrutiny to conflict-of-interest disclosures — and with good reason, given that the general partner occupies both sides of the transaction. How the industry addresses that tension will ultimately determine whether the continuation fund endures as a feature of the private capital toolkit, or serves as a cautionary chapter in the history of financial innovation.

M&A Market Activity

U.S. deal volume grew by 4.1 percent in the first two months of 2026 as compared to the same period last year. Primary macroeconomic drivers of the uptick include a friendlier financing environment, with stabilizing interest rates and strong private credit availability, elevated levels of private equity dry powder, and strategic buyers looking to gain rapidly evolving new technologies and capabilities through acquisition. Barring unexpected policy changes or broader market volatility, the increase in deal volume, and a more pronounced increase in deal value, is expected to continue throughout fiscal year 2026.

The Columbus M&A market saw deal volume remain flat in February as compared to the prior year, however several large acquisitions were completed during the period, including Huntington’s acquisition of Cadence Bank, Park National Corporation’s acquisition of First Citizens Bancshares, and Advanced Drainage Systems Inc.’s acquisition of National Diversified Sales Inc., all of which were previously announced. Additionally, Installed Building Products completed multiple strategic acquisitions during the month.

Deal of the Month

On February 5, 2026, New York-based 4×4 Capital, a growth-oriented investment firm that partners with businesses across the consumer sector, announced its acquisition of Bob Evans Restaurants from Golden Gate Capital. Founded on a farm in Rio Grande, Ohio in 1948, Bob Evans Restaurants operates more than 400 locations across 18 states, and its dedication to community engagement through farming and neighborhood initiatives is a cornerstone of its identity.

“We are proud of what we accomplished in partnership with Golden Gate Capital and excited to begin this next chapter with 4×4’s hands-on partnership. Together, we look forward to investing in and enhancing our operations, guest experience, and brand—with a continued focus on stability, partnership, and long-term value creation,” said CEO Mickey Mills.

“What truly sets the Bob Evans brand apart is its distinctive hospitality, welcoming ambiance, and fresh, flavorful food—delivering real value for the whole family. We look forward to partnering with Mickey and the team to maximize long-term growth,” commented Gustavo Assumpção, Executive Board Chair and 4×4 Co-Founder & Partner.

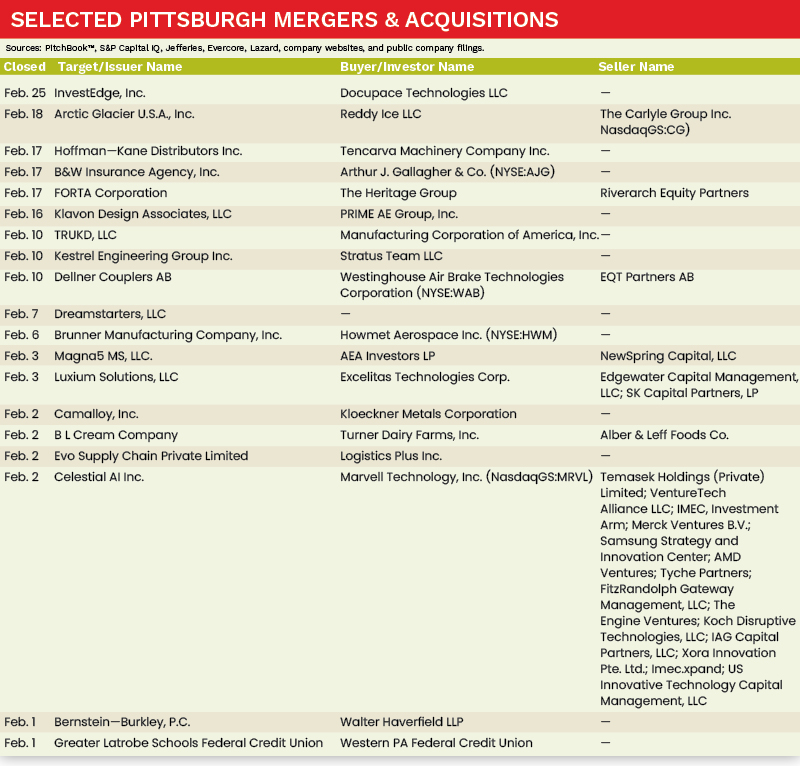

Sources: PitchBook™, S&P Capital IQ, Jefferies, Evercore, Lazard, company websites, and public company filings.

Daniel Bowman is a Director & Principal at MelCap Partners, LLC, a middle-market investment banking advisory firm. For more information on MelCap Partners, please visit www.melcap.com or email [email protected].