The outlook for M&A in 2026 is strengthening as market conditions continue to stabilize and confidence among both corporate buyers and private equity firms rises. After several years of volatility marked by supply chain disruptions, inflation, and higher interest rates, dealmakers now see a clearer environment for negotiation and valuation. Surveys from Deloitte and the Wall Street Journal show broad expectations for growth in both deal count and deal value, reflecting a market that is preparing for increased activity across the middle market and large-cap segments. With financing conditions improving and strategic priorities shifting toward transformation and portfolio optimization, 2026 is shaping up to be a year of renewed momentum.

This optimism follows a 2025 market defined by a growth in deal value, a resurgence of large transactions, and more disciplined but active private equity deployment. Improved access to credit, multiple Federal Reserve rate cuts, and greater clarity around tariff implications played major roles in unlocking activity. Buy-side M&A activity grew as strategic acquirers leaned on M&A to accelerate digital transformation, including adoption of AI technologies, consolidate for scale, and divest non-core operations. Private equity investors continued to prioritize businesses with recurring revenue, service-driven models, and minimal tariff exposure. Cross-border interest in North America also strengthened, while more than $1 trillion in private equity dry powder maintained strong demand for high-quality assets. These forces created the foundation for the recovery now fueling expectations for 2026.

From a macroeconomic perspective, the setup for 2026 is notably more supportive than the environment of the past few years. The Federal Reserve delivered multiple rate cuts, and continual cuts remain possible, helping bring debt markets back into balance and lowering the cost of capital. Market sentiment has also improved as companies adjust to post-pandemic, supply-chain shocks, and inflation realities and view M&A as the fastest path to transformation or operational retooling. Better visibility into trade policy, and ongoing demand for digitalization and sustainability initiatives are expected to further strengthen deal feasibility. Overall, the macro environment is shifting from one of uncertainty to one of alignment, allowing buyers and sellers to engage on valuation with more conviction.

Private equity enters 2026 with even greater urgency and opportunity. Exit activity rebounded in 2024 and 2025 and is expected to broaden further as market sentiment improves. The U.S. now holds nearly 13,000 private equity-backed companies, and a significant share of these assets are aging, with more than 30 percent held for seven years or longer. Coupled with rising public markets and expanding exit windows, firms are encouraged by the potential to hit value targets earlier and monetize assets at stronger multiples. Deal flow through October 2025 already approached the one-trillion-dollar mark, with platform LBOs reaching their highest value since 2021. Looking ahead, private equity investors expect an increased emphasis on exits, improved exit opportunities, and a growing focus on mid-market deals and sector specializations. Financing is becoming more accessible, and the pressure to deploy capital remains high.

Taken together, these dynamics point to a more robust M&A landscape in 2026. The year is expected to be shaped by sustained private equity activity, a deeper pool of exit-ready assets, and strong appetite for transformative acquisitions in sectors, such as in technology, industrials, healthcare, and energy. International buyers are likely to remain active as they seek stability and diversification in U.S. markets. With valuations more stable and financing conditions improving, the balance between risk and return is becoming more attractive for both buyers and sellers. Deal pipelines are full, and market participants widely expect negotiations to convert into closed transactions at a faster pace. If current momentum holds, 2026 could mark a meaningful expansion in both deal count and deal value, driven by clearer macro conditions, private equity urgency, and ongoing sector-level transformation.

M&A Market Activity

U.S. deal volume in November 2025 increased by 12.3 percent as compared to October, with YTD volume 4.6 percent above the total transactions for the prior YTD period. 2025 is on track to surpass overall 2024 activity, highlighting a meaningful pickup in transaction momentum. Broad participation from both strategic and private equity buyers points to increasing confidence and a more optimistic outlook for dealmaking to finish out the year.

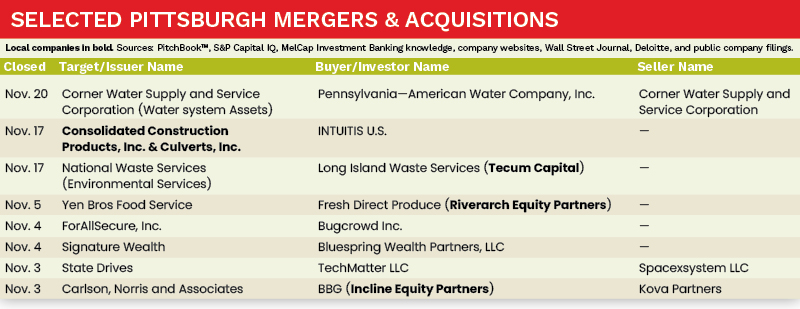

The Pittsburgh M&A market experienced a 38.5 percent decrease in activity in November 2025 compared to the same period in 2024.

Deal of the Month

On November 17th, Ohio-based Consolidated Construction Products (CCP) Inc. and Pittsburgh-based Culverts Inc. (collectively “Consolidated” or the “Company”), regional leaders in the supply of concrete, drainage, and masonry products, were acquired by INTUITIS U.S.

Operating as one combined organization, Consolidated is comprised of two primary divisions, whereby CCP is the Company’s concrete wholesale supply division and Culverts is the Company’s drainage division. CCP is headquartered in Andover, Ohio, and is comprised of six physical distribution locations in Michigan, Kentucky, Pennsylvania, and Ohio — and serves an eight-state area throughout the Great Lakes and surrounding regions. Culverts is based in the Pittsburgh, Pennsylvania region, and sells corrugated pipe, fittings and other specialty drainage products.

INTUITIS acquires controlling interests or significant minority interests alongside the management team in well-established companies — and has concerted experience in both the concrete and drainage industries. INTUITIS has acquired majority control of Consolidated, while certain members of the Company’s leadership team have maintained a reasonably significant minority interest moving forward, highlighting the optimism surrounding the next phase of growth this partnership will bring.

Sources: PitchBook™, S&P Capital IQ, MelCap Investment Banking knowledge, company websites, Wall Street Journal, Deloitte, and public company filings.

Evan J. Lyons is a Director & Principal at MelCap Partners LLC, a middle-market investment banking advisory firm. For more information on MelCap Partners, please visit www.melcap.com or email [email protected].