Although many people in the M&A community like to talk about valuations in the form of multiples of EBITDA, revenue, annual recurring revenue, or other metrics, ascribing a value to an enterprise is much more complicated than multiplying a couple of metrics. Buyers try to estimate the future earnings potential of businesses by taking into consideration all aspects of the company, including product differentiation, customer base, end market trends, the strength of the management team, and numerous other aspects of the organization and the markets in which it participates. Historically, particularly for traditional manufacturing businesses with steady growth, recent sales and earnings have been viewed as the easiest and most accurate way to predict future results.

However, because companies have been operating for several years in a unique environment caused by the COVID-19 pandemic, buyers are more skeptical that recent performance is an indicator of what is to come. Across all industries, buyers are scrutinizing all forecasts much more granularly and not just those with “hockey stick growth,” in order to get comfortable that historical results over the past few years were not temporary highlights caused by unique market conditions. Instead of accepting forecasts with moderate (~5 percent) growth and consistent margins, buyers are diving deeper to understand forecasting assumptions and stress test them against worst-case scenarios.

Because of this, potential sellers must ensure that they have spent adequate time forecasting and have used data-driven assumptions and market analysis to drive projections. During buyer due diligence, sellers and their advisers should be prepared to address and explain their methodology and confidently address buyer questions and concerns. Doing so will drive buyer interest and valuation multiples.

While the primary impetus for this change in buyer perspective stems largely from the pandemic and other macroeconomic factors like interest rate increases and complex geopolitical conditions, we expect that this aspect of buyer assessment will become a regular step in the deal process for the foreseeable future.

M&A Market Activity

U.S. deal volume declined by approximately 13 percent in March 2024 as compared to the prior month, and YTD volume decreased by approximately 22 percent as compared to the prior year. That said, transaction value remains near historical highs, as private equity firms and strategic acquirers have significant liquidity and are willing to pay premiums for high-quality assets.

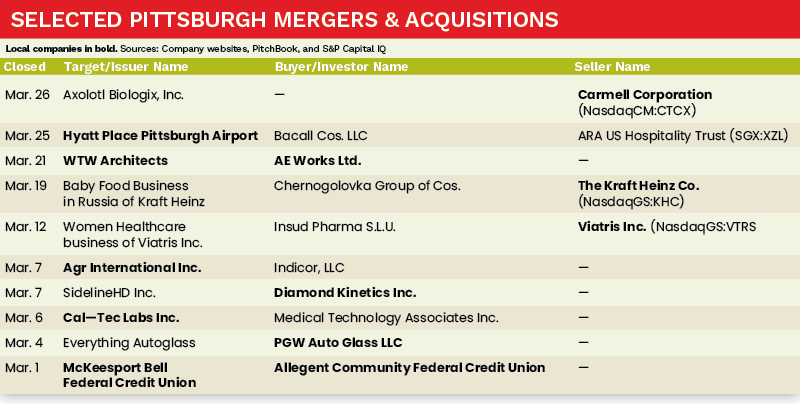

The Pittsburgh M&A market saw relatively flat of deal volume in March of 2024 as compared to the prior month, which continued the trend of lagging behind prior year activity. March 2024, however, saw several noteworthy transactions completed, by both strategic acquirers and private equity firms. Diamond Kinetics, AE Works, PGW Auto Glass and Allegent Community Federal Credit Union all completed strategic acquisitions, while companies like Hyatt Place Pittsburgh Airport, WTW Architects, Cal-Tec Labs, Viatris and the Kraft Heinz Co. saw successful exits during the period.

Deal of the Month

The deal of the month for March 2024 in Pittsburgh is Agr International’s sale to Indicor. Agr International is a provider of quality and process control technologies serving beverage packaging customers globally. The company provides technology and services that support global glass and plastic packaging customers in ensuring their quality, productivity, and sustainability goals are met. Agr is well positioned to capitalize on sustainability tailwinds, with patented technology that enables the use of recycled materials in the manufacturing process.

As noted by Doug Wright, CEO of Indicor, Agr is a “terrific business with clear niche market leadership, mission-critical solutions, deep customer intimacy, and a commitment to supporting their customers’ quality and sustainability needs. This acquisition demonstrates Indicor’s disciplined capital deployment strategy of partnering with high-quality, leading businesses that compound Indicor’s long-term financial returns.” ●

Daniel Bowman is a Director with MelCap Partners, LLC, a middle-market investment banking advisory firm. For more information on MelCap Partners, please visit www.melcap.com or email [email protected].