The domestic M&A market is in a state of great disparity. Valuations from buyers receded to pre-pandemic levels while sellers continue to expect the lofty valuations seen in the latter portion of 2020 and throughout 2021. On one hand, buyers, who are sitting on near-record amounts of deployable dry powder, have demonstrated a willingness to pay healthy multiples for high-quality companies with an entrenched position in the marketplace. On the other hand, a volatile job market, elevated inflation and higher borrowing rates have left otherwise acquisitive companies at a standstill. The result is a best of times, worst of times scenario.

Best Of Times

Financially stable buyers — companies with high levels of deployable dry powder and low levels of debt — continue to be acquisitive while paying full multiples for healthy businesses that possess strong customer relationships and the consistent ability to generate cash flow. Sellers who have performed well are receiving additional attention as the supply of high-quality businesses is down.

Moreover, financial sponsors are sitting on record amounts of capital. According to Preqin, private equity dry powder totaled $3.7 trillion at the end of 2022. These record-high levels are expected to continue in 2023, and healthy businesses that are primed for sale can continue to expect meaningful attention from the buyer universe.

Worst Of Times

Inflation, which rose to a 40-year high this past year, continues to erode purchasing power in the marketplace. As a result, buyers are forced to reconsider their leveraged investing strategies while sellers evaluate whether it’s the right time to pursue a sell-side transaction. Companies that have consistently demonstrated sustainable profits are able to weather the storm, while companies with an ownership structure committed to an exit are willing to accept lower valuations stemming from the declining market trends.

With the cost of borrowing on the rise, aggressive companies have remained acquisitive, signaling a belief that companies being acquired will outperform high borrowing rates, while conservative companies are holding out for a return to “normalized” levels. Acquirers continue to demonstrate a flight to quality companies as targets for purchase.

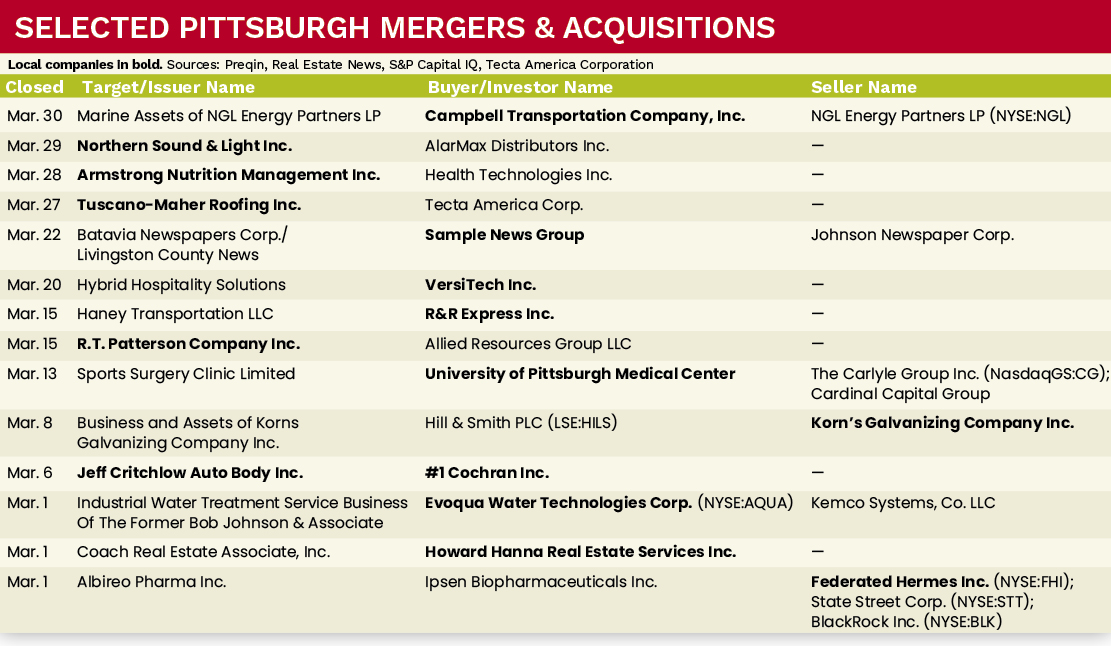

M&A Market Activity

National deal volume maintained pace in March 2023, as compared to the prior month. U.S. M&A deal volume for Q1 2023 was 9 percent lower compared to Q4 2022.

The Greater Pittsburgh M&A market experienced an increase in March 2023, as the area’s deal volume was 25 percent higher as compared to February 2023. March 2023 also saw several noteworthy transactions in the Northeast Ohio region. Campbell Transportation Company, Sample News Group and VersiTech completed strategic acquisitions within the month. To continue on expansion strategy, Pittsburgh-based Howard Hanna Real Estate Services merged with Coach Real Estate Associates. The new company will be able to serve the upstate and downstate New York markets.

Deal of the Month

On March 27, 2023, Tecta America Corp., the largest roofing contractor in the U.S., acquired Saltsburg-based Tuscano-Maher Roofing. TMR provides re-roofing, service and maintenance, and new construction roofing and sheet metal services for local and state municipalities, property owners and property managers. Dave Reginelli, Tecta’s president and CEO, said of the acquisition, “We are thrilled to welcome TMR to our family of companies. Mike Maher, Marty Nalevanko, Joe Slapinski, and the rest of the TMR team share in our belief that working safely, focusing on our people, and providing the best possible service to our customers allows for continued long-term partnership and success.” The acquisition adds to Tecta’s growing presence of over 90 locations across the nation. ●

Al Melchiorre is president and founder of MelCap Partners, LLC, a middle-market investment banking advisory firm. For more information on MelCap Partners, please visit www.melcap.com or email [email protected].